Business insurance in Canada | Insurance Business Canada

Insurance plan Enterprise delves further into how organization insurance coverage in Canada operates in this short article. We will give you a rundown of the distinctive policies readily available and response the most common business insurance plan-associated questions you may well have. For the insurance coverage specialists who regularly visit our site, this can provide as an exceptional short article for purchasers of yours that have issues about Canadian business insurance.

Company insurance plan is an umbrella expression for a array of procedures made to safeguard enterprises from the distinctive pitfalls they are uncovered to. It serves as a form of a financial cushion that enables companies to recoup their losses a lot quicker just after a unexpected and unlucky occasion.

But as just about every business enterprise faces a exclusive set of dangers, the type of coverage they call for likewise varies. For this reason, business coverage firms in Canada offer you companies a tailored variety of guidelines that matches their certain requirements.

There is no law in Canada mandating business enterprise entrepreneurs to take out small business coverage – until, of study course, it is for a business vehicle, which is a authorized prerequisite for all Canadian motorists just before they can be permitted to hit the street.

Some customers and stakeholders may perhaps also demand you to obtain specified types of guidelines for a offer to observe as a result of – and for great motive. Having the proper business insurance coverage guidelines in area allows secure you and your consumers in opposition to the financial impact of unexpected losses.

While not compulsory, enterprise insurance plan can be a wise investment for several Canadian entrepreneurs since of the sort of defense it gives. But as just about every enterprise is exposed to a unique established of pitfalls and issues, there is no single business enterprise insurance coverage in Canada that can address just about every will need. This is why company insurance plan suppliers throughout the country offer you a various variety of coverages.

Below are some of the most important company insurance policy policies that Canadian firms really should consider, according to field authorities.

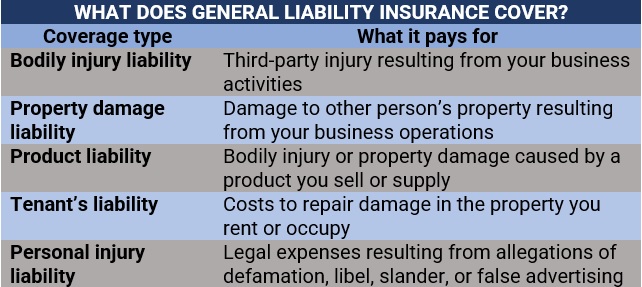

1. Industrial normal legal responsibility insurance plan

A detailed industrial normal liability insurance plan, also identified as CGL insurance policies, covers you for third-get together injuries and property damage that manifest owing to negligence in your business enterprise routines. It also pays out for statements of damage ensuing from a faulty operate or solution, although this might also be included by standalone product or service liability coverage.

Typical legal responsibility insurance plan is mostly intended to protect you from lawsuits. It can also go over conditions that relate to libel or slander. CGL insurance pays for lawful fees, damages, and out-of-court settlements up to the restrictions of your policy.

The table underneath sums up the diverse sorts of protection typical legal responsibility insurance coverage gives:

2. Experienced legal responsibility insurance plan

Also referred to as problems and omissions (E&O) insurance, professional legal responsibility insurance coverage safeguards your business from claims of economic losses from shoppers due to a provider you have provided. These include things like lawsuits alleging your company of the next:

-

- Carelessness

- Misconduct

- Giving bad tips

- Lacking deadlines

- Failing to supply merchandise and solutions as promised

One particular essential matter to take note is that you do not will need to dedicate an genuine error to be slapped with a claim. Your consumer only desires to understand that you had been negligent for them to be equipped to file a declare.

If your business enterprise is involved in the pursuing, experienced liability insurance coverage could be a good investment decision:

-

- Supplying guidance or companies in exchange for a fee

- Giving or establishing products and solutions or units

This sort of coverage is also named malpractice insurance policies in sure professions, such as medical practitioners and attorneys. Some occupations are also expected to consider out professional legal responsibility insurance policy to be equipped to observe lawfully. These incorporate accountants in Ontario.

You can look at out our comprehensive guidebook on expert indemnity insurance plan to study additional about this form of organization coverage.

3. Solution liability insurance

Products legal responsibility insurance plan protects you against claims of bodily personal injury or property hurt induced by a products your organization sells, manufactures, or distributes. It handles damages resulting from defective design and style, producing, and internet marketing, together with incorrect labelling and security warnings.

The form of coverage product or service legal responsibility supplies is usually included less than typical legal responsibility insurance plan procedures. One crucial point to bear in thoughts, on the other hand, is that products legal responsibility insurance policies does not address company-linked statements. For these, you will will need to just take out expert legal responsibility insurance.

Item legal responsibility policies are advisable for any company that sells or manufactures a solution, which includes meals products. Vendors, the two on the net and in brick-and-mortar destinations, are amongst all those who can advantage from this style of coverage.

4. Professional property insurance plan

Professional house insurance coverage – also identified as business constructing or business enterprise assets insurance policy – addresses bodily reduction or injury to your property and its contents prompted by an external occasion, like hearth, theft, and vandalism. Your business enterprise needs this style of protection if:

-

- You have an business office or commercial place

- You very own or lease a commercial making, equipment, or inventory

- Your setting up residences computer systems, components, or machinery that you use for business

- You have portable electronics – which includes laptops, tablets, and cellular telephones – for your business enterprise

- You conduct small business off-web page

Industrial assets insurance coverage usually provides the pursuing safety:

-

- Setting up protection: Pays out the value to replace or maintenance injury to a property your enterprise owns if this is brought about by a lined peril.

- Tenant enhancement coverage: Handles bodily renovations and updates you make to a home that your enterprise rents which are not able to be simply taken off these kinds of as paint, carpeting, and lighting.

- Inventory protection: Pays out alternative or repair service prices of your items and inventory if these are damaged by an insured event.

- Devices and fixtures protection: Covers the value to swap or maintenance equipment, fixtures, and furnishings that were being dropped or harmed due to a protected peril.

- Electronics protection: Insures digital equipment that you use for company if they are weakened or stolen inside of or outside the house of your office environment.

5. Professional auto insurance policies

As the name indicates, commercial auto insurance – also referred to as commercial car or organization auto insurance – addresses cars that you use for your enterprise. These consist of:

-

- Organization cars and trucks

- Trailers

- Vans

- Vans

Each individual car that you use to transportation items, devices, elements, equipment, and staff should carry a professional auto insurance plan.

Business car or truck insurance delivers the very same protection as private auto procedures. Provinces and territories have their individual principles and regulations when it will come to required coverage, but there are similarities. These are:

-

- Third-party legal responsibility (TPL): Covers the price tag of lawsuits if a motorist is responsible for an incident that brings about bodily harm, death, or assets problems.

- Immediate payment residence injury (DCPD): Relevant in Ontario, Québec, Nova Scotia, New Brunswick, and Prince Edward Island, this coverage handles damages to the automobile and its contents ensuing from an accident with a further insured car or truck as lengthy as the policyholder is not at fault.

- Accident added benefits (AB): Pays out for medical treatment options and earnings replacement if the policyholder is injured in an incident, no matter of who is at fault. It also handles funeral bills.

- Uninsured automobile/motorist (UM): Coverage kicks in if the policyholder or their passenger is hurt or killed by an uninsured driver or in a hit-and-run incident. It also covers damages to the car.

This variety of business coverage can be completely priceless.

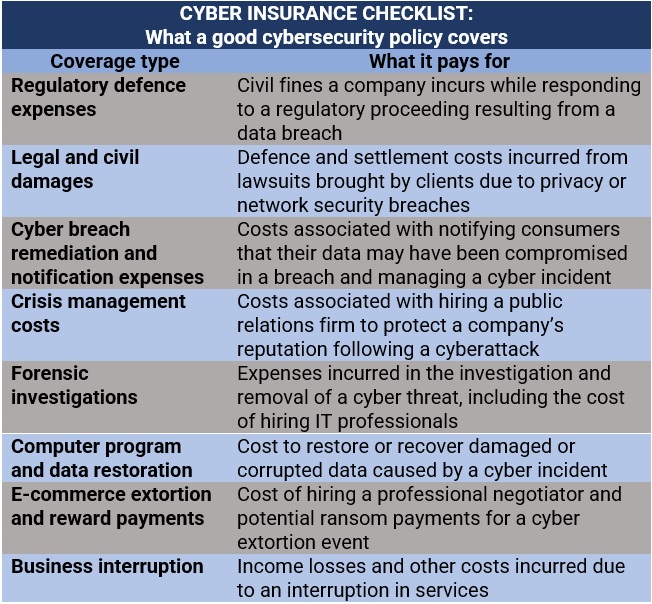

6. Cyber legal responsibility insurance policy

Cyber liability insurance plan is created to safeguard your business in opposition to financial losses ensuing from cyber incidents. In its cyber insurance plan guide, the IBC detailed the kinds of protection a excellent cybersecurity insurance plan coverage delivers. These are in-depth in the table underneath.

Some industries are extra vulnerable to a cyberattack than other individuals. Our hottest cybersecurity tutorial reveals which industries in Canada are most in need of cyber protection.

7. Directors’ and officers’ (D&O) legal responsibility insurance plan

D&O liability insurance policy, also identified as administration legal responsibility coverage, is created to defend the directors and senior administration of a corporate or non-gain group versus money losses ensuing from organization-linked lawsuits. This variety of coverage pays out for monetary losses from these authorized steps, like defence prices, settlements, and fines.

D&O insurance coverage arrives in a few most important styles, also referred to as insuring agreements:

-

- Facet A: Addresses “non-indemnifiable losses” or individuals conditions exactly where the company or company are not able to indemnify its directors or officers, either owing to personal bankruptcy or mainly because they are not lawfully authorized to do so.

- Facet B: Reimburses a company immediately after it has compensated a director or other senior management for a reduction, including defence fees, settlements, or judgments. This is the most popular style of insuring arrangement.

- Side C: Delivers immediate protection for a business when both equally the company and its administrators and senior management are named in a lawsuit.

If you are interested in discovering much more about how this form of coverage operates, you can check out out our thorough D&O insurance plan tutorial.

8. Business interruption insurance

Business enterprise interruption insurance policies, also referred to as BI or business enterprise cash flow insurance policy, supplies fiscal protection for the losses your business sustains due to the disruption of your operations ensuing from an insured function. It pays out the functioning expenses though the organization temporarily shuts down. These costs contain:

-

- Prospective earnings

- Mortgage or lease on business house

- Company personal loan repayments

- Personnel salaries

- Taxes

Some policies also deliver coverage for supplemental expenses associated to the closure these as people incurred for location up of a short term place or the instruction of staff members to use new machines.

9. Daily life insurance policy

Life coverage may possibly not be among the the standard procedures that appear into intellect when thinking about business enterprise insurance plan in Canada, but company-owned daily life policies present companies with a number of added benefits. These incorporate:

Funding buyout agreements

A buyout everyday living insurance policies arrangement is created to guard a enterprise in the party a co-owner dies. In these an arrangement, the death profit is made use of to fund acquire-market transactions. This frequently happens when the remaining homeowners are not fascinated in obtaining the deceased’s loved ones stay associated in the small business and the loved ones furthermore shows no desire in executing so.

Crucial worker coverage

Company-owned daily life insurance plan can cover a important crew member and provide economic benefit to your enterprise at the time of the employee’s death. It is notably beneficial for corporations that rely on particular workers for essential tasks. The payout is intended to give monetary assistance as the enterprise goes through a changeover period to discover and coach a replacement.

Estate equalization

Life insurance plan can be made use of if you want to move alongside a small business with a number of beneficiaries to a solitary spouse and children member. The process, named estate equalization, enables you to bequeath the complete business to a single relatives member when nevertheless leaving something for their other dependents.

If you want to know the other approaches companies can use lifetime insurance policy to their benefit, you can check out our comprehensive guidebook to company-owned lifestyle insurance policy.

As with other sorts of insurance coverage, the total of coverage your organization wants relies upon on a range of things that may perhaps be exclusive to your operations. The finest bet, according to professionals, is to choose out as substantially protection as you can afford. Going for the most economical selection is by no means highly recommended as you may possibly afterwards uncover out that it may not be in a position to offer more than enough defense for you to manage functions.

When not necessary, getting out organization insurance coverage yields a ton of gains. Just one of the most clear pros is the fiscal defense these types of guidelines give when sudden losses happen. These include things like organic and person-created disasters and costly litigation that can take a enormous chunk out of your profits. Owning the suitable types of coverages can assistance your small business get better more rapidly.

Company insurance policies in Canada is also tax deductible. You can claim the cost of your premiums versus your taxable profits, minimizing the amount of money you require to spend.

A further advantage of having company insurance plan is that it boosts your company’s trustworthiness as most customers and stakeholders like operating with corporations that they are conscious are fiscally guarded.

Small business coverage, nevertheless, is just 1 way of mitigating your company’s hazards. Nonetheless, the ideal way for you to guard your business’ property and funds is by pairing the ideal insurance policy protection with great hazard administration techniques.

The require for company insurance policies is not special to Canadian enterprises. Corporations across the globe can maintain some amount of economic protection by investing in the right form of insurance coverage. Uncover out how enterprises can use small business insurance to deal with worldwide issues in this manual.

Do you imagine it is sensible to invest in enterprise insurance coverage in Canada? Which types of coverages are necessary and which kinds can you afford to pay for to forego? Share your views in our reviews portion below.

:quality(70)/d1hfln2sfez66z.cloudfront.net/02-02-2023/t_832fc9813d3741189856dfd7da126358_name_Car_Insurance_Increase_transfer_frame_627.jpeg "Car insurance rate hikes are here in Washington state – KIRO 7 News Seattle")